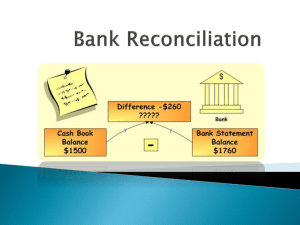

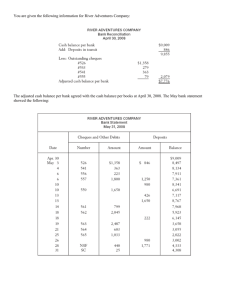

CAF 1 – Bank Reconciliation Statement Bank Reconciliation Statement - 07 Page | 1 CASH AT BANK Cash book / Bank book Bank statement / Pass Book Difference The cash book provides us with the balance we have in our bank account and for each bank account separate record is maintained. Normal / Favourable balance Debit Overdrawn / Overdraft / Unfavourable balance Credit The bank also provides us with a statement of our account. This statement records transactions from bank point of view, therefore, debits and credits are reversed in it. Normal / Favourable balance Credit Overdrawn / Overdraft / Unfavourable balance Debit In ideal situation, the balance from both should match. However, due to errors and omissions and due to timing differences, the balance may differ which needs to be reconciled in order to ensure that there is no embezzlement etc. . Adjustment in Errors and omissions Errors and omissions (items not yet recorded) in cash book Errors and omissions (items not yet recorded) in bank statement Timing difference Un-presented items: these are items credited in cash book but will be debited by bank after period end Uncredited items / un-cleared items: these are items deposited in bank account but bank will credit them after the year end. Possible reason of differences Cash Book Bank Reconciliation Statement Bank Reconciliation Statement Bank Reconciliation Statement . Adjusted balance This is the balance as per cash book after all the errors and omissions in cash book have been corrected and adjusted. This is also called true balance of cash and this is the amount used in statement of financial position. This figure is also used as starting point for preparing bank reconciliation statement. © kashifadeel.com CAF 1 – Bank Reconciliation Statement BANK RECONCILIATION STATEMENT Balance as per cash book (adjusted) Page | 2 Normally, debit Un-presented items Un-cleared, un-credited items Debit Credit Error by bank: bank wrongly debited Error by bank: bank wrongly credited Credit Debit Items Balance as per bank statement Normally, credit . Particulars Ref. Balance as per cash book (adjusted) Un-presented cheques Un-credited cheques Specimen Dr. (Rs) XXX XX Cr. (Rs) XX Error by bank Balance as per bank statement Total XX XXX XX XXX XXX . SYLLABUS Reference Content/Learning outcome Bank reconciliation and related adjustments Understand the need for a bank reconciliation Identify the main reasons for differences between the cash book and bank LO2.3.2 statements. Prepare a bank reconciliation statement in the circumstance of simple and well LO2.3.3 explained transactions. Correct cash book errors and post journal entries after identifying the same in LO2.3.4 bank reconciliation statement Proficiency level: 2 Testing level: 2 B3 LO2.3.1 Past Paper Analysis A14 S15 A15 S16 14 09 14 A16 10 S17 09 A17 - S18 08 Latest update: April 2020 A18 - S19 - A19 08 S20 01 CAF 1 – Bank Reconciliation Statement PRACTICE Q&A Sr.# 1H 2C 3C 4H 5H 6H 7H 8C 9C 10C 11H 12H 13C 14C Description Marks Sohrab – BRS 04 Jabbar – Cash book and BRS 07 BRS reverse calculations 06 Al – Murtaza 10 ABC Textiles 15 Mr. Mubarak 15 Ranjha Enterprises 09 Galaxy Enterprises 14 Eden Garments 10 Comforts Travels 09 A Company 06 Badami Enterprises 14 Unique Traders - BRS from last month BRS and current 08 month Bank Book and Bank statement Lamda Establishment 08 © kashifadeel.com Reference ST ST QB QB QB QB PE A15 PE S16 PE A16 PE S17 QB PE S15 PE S18 PE A19 Page | 3 CAF 1 – Bank Reconciliation Statement QUESTION 01 On 30 June the cash account of Sohrab’s business showed a balance at bank of Rs. 1,500,000. Page | 4 The bank statements showed that cheques for Rs. 70,000, Rs.90,000 and Rs.100,000 had not been presented for payment and that lodgments totaling Rs.210,000 had not been cleared. The balance on the bank statement at 30 June was Rs. 1,550,000. Required Prepare a bank reconciliation. (04) QUESTION 02 The balance in Jabbar’s cash account at 30 June showed an asset of Rs.1,660,000. His bank statement showed an overdraft of Rs.450,000. On reconciling the cash account he discovers the following. (a) The debit side of the cash account had been undercast by Rs.200,000. (b) A total on the receipts side of the cash account of Rs.2,475,000 had been brought forward as Rs.4,275,000. (c) A cheque received by Jabbar for Rs.220,000 had bounced. (d) Bank charges of Rs.184,000 had been omitted from the cash account. (e) Un-presented cheques totalled Rs.520,000 and un-cleared lodgements Rs.626,000. Required Prepare a bank reconciliation. (07) QUESTION 03 A company receives a bank statement showing a credit balance of Rs.7,400,000. On investigation, its accountant discovers that the bank statement does not show cheques received from customers for Rs.16,200,000 and banked, or cheque payments to suppliers for Rs.18,500,000. The bank statement also shows bank charges of Rs.250,000, which have not yet been recorded in the ledger. Required What is the current balance on the cash book? (This is the balance on the Bank account in the main ledger.) (06) QUESTION 04 Following information has been collected from the books of Al-Murtaza Company, as at August 31, 2013: (a) (b) (c) Balance as per bank book Rs. 272,178 Cash balance on bank statement Rs. 227,522 Cheques outstanding on August 31 were as follows: Cheque No. Rupees 670 13,353 679 14,152 690 17,108 996 3,535 997 14,430 999 23,629 Latest update: April 2020 CAF 1 – Bank Reconciliation Statement (d) The company made the following payments into the bank in the last week in August but these had not yet appeared on the bank statement. Rupees 83,250 144,641 (e) The following matters have been discovered. (i) Receipt of Rs. 15,000 was erroneously recorded on the credit side of the bank book. (ii) A payment of Rs. 12,480 was erroneously recorded on the debit side of the bank book. (iii) The credit side of the bank book has been over casted by Rs. 4,800. (iv) The bank statement showed an amount collected by the bank but not shown in the cash book in the amount of Rs. 87,188. Required: Prepare the bank reconciliation as at 31 August. (10) QUESTION 05 While reconciling the bank statement with the cash/bank book of ABC Textiles for the year ended December 31, 2013, you noted the following: Rupees (i) Balance as per bank statement at December 31, 2013, overdrawn 806,436 (ii) Cheques drawn but not presented till December 31, 2013 377,784 (iii) Mark-up on overdraft charged by the bank on January 2, 2014 was 118,686 recorded in the cash/bank book on December 31, 2013 (iv) Collections made on December 30 and 31, 2013 were not lodged 250,600 with the bank till January 3, 2014 (v) A bill which was due on December 29, 2013 was sent to the bank for collection on December 28, 2013, and entered in the cash/bank book. 196,500 However, the proceeds were credited by the bank on January 1, 2014 (vi) Subscription for a magazine was paid by the bank, as per the autodebit instructions, on December 1, 2013. This transaction has not 3,144 been recorded in the cash/bank book so far (vii) A time-barred cheque was replaced with a new cheque on December 30, 2013 and entered in the cash/bank book without the previous 5,000 cheque being cancelled / reversed. Both the cheques are included in (ii) above (viii) Discount allowed on prompt payment to customers has been 10,500 included in the cash/bank book (ix) A cheque received on December 21 was erroneously recorded on the 7,500 credit side of the cash/bank book (x) A cheque issued to a supplier was time-barred as of January 2, 2014 25,000 (xi) A cheque for Rs. 125,000 drawn by the company to pay for a new 12,500 item of plant had been mistakenly entered in the cash/bank book as (xii) A cheque issued by the company has been entered in the credit 13,200 column of the bank statement Required: Prepare a bank reconciliation statement as at December 31, 2013 and identify the amount to be carried to the statement of financial position as “Cash at Bank”. (15) © kashifadeel.com Page | 5 CAF 1 – Bank Reconciliation Statement QUESTION 06 Mr. Mubarak is a sole trader and carries on business under the name “Mubarak & Company”. The balance on his cash book at 31 December 2013 did not agree with the balance as per the bank statement which shows a credit balance of Rs. 367,500. Page | 6 An examination of the cash book and bank statement disclosed the following: (i) A deposit of Rs. 49,200 made on 29 December 2013 had been credited by the bank on 1 January 2014. (ii) Bank charges of Rs. 1,700 have not been entered in the cash book. (iii) A debit of Rs. 4,200 appeared on the bank statement for an unpaid cheque which has been returned marked “out of date”. The cheque was re-dated by his customer and paid into the bank again on 3 January 2014. (iv) A standing order for payment of an annual subscription amounting to Rs. 1,000 has not been entered in the cash book. (v) On 26 December 2013, Mr. Mubarak had given the cashier a cheque for Rs. 10,000 to pay into his personal account at the bank. The cashier deposited it into the business account by mistake. On 27 December 2013, a customer had made an online transfer of Rs. 49,900 in payment against goods supplied. The advice was received and recorded in the cash book on 2 January 2014. (vi) (vii) On 30 September 2013, Mr. Mubarak entered into a hire purchase agreement and issued a standing order to the bank to pay a sum of Rs. 2,600 on the 10th day of each month, commencing from October 2013. No entries have been made in the cash book for these payments. (viii) A cheque for Rs. 36,400 received from Mr. Bashir had been entered twice in the cash book. (ix) Cheques issued amounting to Rs. 467,200 had not been presented to the bank for payment until after 31 December 2013. (x) A customer who owed Rs. 20,000 and was entitled to a cash discount of 2½% paid a cheque for the net amount on 10 December 2013. The cashier erroneously recorded the gross amount in the bank column of the cash book. (xi) Dividend collected by the bank amounting to Rs. 12,000 has not been recorded in the cash book. (xii) A cheque of Rs. 243,000 received from Mr. Bilal was deposited in the bank but entered in the cash book as Rs. 234,000. Required: (a) Prepare a bank reconciliation statement as on 31 December 2013. (b) Prepare necessary journal entries in the books of Mubarak & Company and determine the correct cash balance that should be reported in the statement of financial position. Also specify the situations in which no adjustment/entry is required. (15) Latest update: April 2020 CAF 1 – Bank Reconciliation Statement QUESTION 07 On 30 June 2015, the bank book of Ranjha Enterprises (RE) reflected a credit balance of Rs. 3,450,000 whereas the bank statement showed an overdraft of Rs. 2,415,000. On scrutinizing the record, following issues were discovered: (i) Cheques deposited in bank in the last week of June 2015, amounting to Rs. 1,550,000 were wrongly credited in the bank book. Out of these, cheques amounting to Rs. 1,050,000 were cleared by the bank in July 2015 whereas a cheque of Rs. 500,000 deposited on 29 June 2015 was dishonoured by the bank on 2 July 2015. (ii) Financial charges on bank overdraft amounting to Rs. 750,000 were recorded in the bank statement. However, review by the Accounts Officer indicated an error and RE recorded the correct amount of Rs. 510,000 in the bank book. The error was corrected by the bank on 10 July 2015. (iii) A cheque issued to a supplier amounting to Rs. 4,005,000 was entered in the bank book as Rs. 4,050,000. However, the bank erroneously recorded the amount as Rs. 4,500,000. (iv) A supplier was issued a cheque of Rs. 125,000 in place of a time barred cheque on 25 June 2015 and was cleared on the next day. However, the cancellation of time barred cheque was not recorded by RE. (v) A payment of Rs. 50,000 through cheque was recorded twice in the bank book. Required: Determine the correct balance that should be reported in the bank book and prepare a statement reconciling the corrected balance with that shown in the bank statement. (09) QUESTION 08 Galaxy Enterprises (GE) maintains a bank account with Zee Bank Limited. Following information pertains to the bank account for the month of January 2016: Bank book Bank statement Balance as at 31 January 2016 (Dr.) Rs. 856,000 (Cr.) Rs. 1,182,500 Other information: (i) Following is the list of outstanding cheques as at 31 January 2016: Cheque no. Date Rupees 111 14-Jul-2015 250,000 444 23-Nov-2015 79,000 666 15-Dec-2015 455,000 777 28-Jan-2016 500,000 Various 31-Jan-2016 1,350,000 Review of outstanding cheques revealed that incorrect payee's name was mentioned on cheque no. 666. Cheque no. 777 was issued to replace cheque no. 666. The difference of Rs. 45,000 represents payment against another invoice. (ii) Cheques outstanding for more than six months are not honoured by banks. © kashifadeel.com Page | 7 CAF 1 – Bank Reconciliation Statement (iii) Details of un-cleared cheques as at 31 January 2016 are as follows: Date Customer’s name Cheque no. Rupees 8-Oct-2015 Zeta Enterprises 1XX 140,000 3-Dec-2015 XYZ Traders 2XX 70,000 26-Dec-2015 ABC & Co. 3XX 63,000 31-Jan-2016 Various customers Various 1,780,000 Cheque no. 1XX was dishonoured on 28 January 2016. Cheque no. 2XX was mistakenly credited by the bank to another party. GE’s account was however credited on 8 February 2016. (iv) A debit of Rs. 135,000 is appearing in the bank statement of January 2016. It represents reversal of a credit given in December 2015 against a post-dated cheque of 1 March 2016 which was mistakenly deposited by GE. (v) A reconciling item of Rs. 9,000 is appearing in the bank reconciliation statement from December 2015. It represents the difference between a cheque of Rs. 54,000 received from a customer and recorded by GE at Rs. 45,000. The error could not be identified in December 2015. Page | 8 (vi) Following debit advices dated 29 January 2016 were received by GE in February 2016: Bank charges amounting to Rs. 8,500. Payments of Rs. 120,000 for annual subscriptions against standing instructions. Required: (a) Compute corrected Bank book balance and prepare necessary journal entries to correct the errors in the Bank book. (11) (b) Prepare a bank reconciliation statement for the month of January 2016. (03) QUESTION 09 Following information has been extracted from the records of Eden Garments (EG), as at 30 June 2016: Rupees Balance as per bank book (debit balance) 760,000 Balance as per bank statement (overdraft) 1,490,850 An examination of the bank book and the bank statement, revealed the following: (i) Outstanding cheques amount to Rs. 3,856,300 and include: a cheque of Rs. 50,000 issued to a supplier bearing an incorrect payee's name. The cheque was returned and recorded on 15 July 2016. a cheque issued to a supplier for Rs. 85,000 (included in above amount correctly) was recorded in bank book as Rs. 58,000. a cheque dated 20 December 2015 for Rs. 4,630 issued for repair of a car was misplaced. The repair charges were paid in cash and the misplacement of the cheque was not recorded. (ii) Un-cleared cheques amount to Rs. 6,460,000 and include: a cheque of Rs. 366,000 received from a customer was returned by the bank as amount in words was not in conformity with the amount in figures. The return was not recorded and the cheque was sent to the customer for replacement. a cheque of Rs. 76,000 received from a customer in settlement of an invoice availing payment discount of 5%. The collection was recorded by EG at gross amount of invoice. Latest update: April 2020 CAF 1 – Bank Reconciliation Statement (iii) An unidentified credit of Rs. 354,000 was appearing in the bank statement. It was found that a customer had made an online transfer to avail 5% discount allowed on payments made by 30 June 2016. (iv) Following debit/credit advices dated 30 June 2016 were received from the bank on 5 July 2016: Bank charges amounting to Rs. 7,850. It has been noted that the bank had over charged EG by Rs. 1,250. Dividend collected by the bank amounting to Rs. 50,000. Payment on EG’s standing instruction of an annual subscription for a magazine amounting to Rs. 12,000. Required: (a) Post relevant transactions to bank book of EG to arrive at the correct bank balance as at 30 June 2016. (07) (b) Prepare a bank reconciliation statement for the month of June 2016 to arrive at the adjusted bank balance as per EG's books. (03) QUESTION 10 The following bank reconciliation statement pertains to Comforts Travels for the month of February 2017: Rupees Balance as per bank statement 3,258,000 Outstanding cheques (869,200) Cheques deposited and under clearance 456,350 Debit advices for bank charges received in March 2017 9,240 Un-reconciled difference (9,000) Balance as per bank book 2,845,390 Scrutiny of the bank book and bank statements revealed the following: (i) Outstanding cheques above include: a cheque of Rs. 37,250. The cheque was recorded in the bank book (and in above reconciliation) as Rs. 32,750. a cheque amounting to Rs. 9,650 which is outstanding since 8 June 2016. Cheques outstanding for more than six months are not honoured by the bank. (ii) Cheques under clearance include a post-dated cheque of Rs. 35,000 received from a customer on 27 February 2017. The cheque was deposited in the bank on 28 February 2017. The date of the cheque was 1 March 2017. (iii) The bank charges include an amount of Rs. 2,500 which was subsequently reversed by the bank. (iv) A page total of payment side of the bank book amounting to Rs. 4,589,000 was carried forward to the next page as Rs. 4,598,000. Required: (a) Post relevant transactions to the bank book to arrive at the correct balance as at 28 February 2017. (05) (b) Prepare a revised bank reconciliation statement for the month of February 2017 using the corrected bank book balance. (04) © kashifadeel.com Page | 9 CAF 1 – Bank Reconciliation Statement QUESTION Page | 10 11 A company receives a bank statement. The balance on its cash book (= bank account in the main ledger) is a debit balance of Rs.1,600,000. In reconciling the cash book balance with the bank statement balance, the accountant discovers that the bank statement does not show cheques received from customers for Rs.8,200,000 and banked, or cheque payments to suppliers for Rs.4,700,000. The bank statement also shows bank charges of Rs.150,000, a direct debit payment of Rs.400,000 and a dishonoured cheque for Rs.300,000. None of these three items which has yet been recorded in the ledger. Required What is the balance on the bank statement? What entries should be made in the company’s ledger accounts when the cash book and the bank statement balances have been reconciled? (06) QUESTION 12 a) State any ten causes of disagreement between the balance as per bank book and the bank statement. (05) b) On 31 December 2014 the bank book of Badami Enterprise (BE) reflected a favourable balance of Rs. 34,000 while the bank statement showed an overdraft of Rs. 1,712,000. On scrutinizing the two records, following discoveries were made: (i) Cheques of Rs. 325,000 issued to suppliers were not yet presented to the bank. (ii) Bank made payment of Rs. 35,000 in relation to e-payment charges on BE’s account. (iii) BE had instructed the bank to transfer interest of Rs. 45,000 earned on a deposit account to its current account. The bank did not transfer the amount till 15 January 2015 whereas the amount had already been recorded in the bank book. (iv) Cheques of Rs. 630,000 received from customers and deposited to the bank had not been credited by the bank. (v) The receipt side of the bank book was overcasted by Rs. 90,000. (vi) The payment side of the bank book was undercasted by Rs. 42,000. (vii) BE made e-payments of Rs. 720,000 to overseas suppliers. However, these payments were not posted to the bank book. (viii) A cheque of Rs. 30,000 drawn in favour of a supplier was recorded in the bank statement as Rs. 300,000. (ix) A cheque of Rs. 65,000 issued to one of the suppliers had been wrongly posted on the receipt side of the bank book. (x) A cheque of Rs. 80,000 received from Mr. Barkat had been entered twice in the bank book. (xi) Dividend of Rs. 54,000 collected by the bank was recorded at Rs. 63,000 in the bank book. (xii) A standing order for payment of annual subscription fees of Rs. 20,000 for a magazine had not been recorded in the bank book. Required: Determine the correct balance that should be reported in the bank book and prepare a bank reconciliation statement reconciling the amended balance with that shown in the bank statement. (09) Latest update: April 2020 CAF 1 – Bank Reconciliation Statement QUESTION 13 Following information has been extracted from the records of Unique Traders: Date 01 05 09 12 18 25 26 28 Bank book for the month of February 2018 Receipts Rupees Date Payments Balance 133,500 03 Salaries Debtors 315,000 05 Utilities Sales 525,000 08 Purchases Rentals 615,000 15 Rental Security deposit 200,000 20 Purchases Advance from customers 182,000 28 Balance Debtors 294,000 Cash deposited in bank 55,000 2,319,500 Cheque X09 X10 X11 X12 X13 Rupees 225,000 352,000 622,000 608,000 71,000 441,500 2,319,500 Bank statement for the month of February 2018 Date Description Cheque Withdrawals Deposits Balance --------------- Rupees --------------01 Balance 127,500 03 Cheque withdrawal X09 225,000 (97,500) 05 Reversal of credited mistakenly 48,000 (145,500) 09 Cheque withdrawal X05 63,000 (208,500) 14 Outward cheque clearing 315,000 106,500 20 Outward cheque clearing 525,000 631,500 22 Cheque withdrawal X10 325,000 306,500 24 Payment – standing instructions 15,000 291,500 25 Outward cheque clearing 615,000 906,500 26 Outward cheque clearing 200,000 1,106,500 26 Transfer (from a debtor) 38,000 1,144,500 27 Cheque returned 200,000 944,500 28 Cheque withdrawal X12 608,000 336,500 28 Cheque withdrawal X13 71,000 265,500 28 Cash deposit 55,000 320,500 28 Bank charges 4,500 316,000 1,559,500 1,748,000 (All amounts appearing in the above bank statement are correct) Bank reconciliation statement as on 31 January 2018 Description Bank book Bank Statement ---------- Rupees ---------Balance (133,500) 127,500 Un-presented cheques: Cheque X05 dated 28 January 2018 (63,000) Cheque X06 dated 31 January 2018 (150,000) Amount mistakenly credited by bank (48,000) Corrected balance (133,500) (133,500) Required: Prepare bank reconciliation statement as on 28 February 2018, showing the correct balance as per bank book and bank statement. (08) © kashifadeel.com Page | 11 CAF 1 – Bank Reconciliation Statement QUESTION Page | 12 14 Lamda Establishment is preparing bank reconciliation statement on 30 June 2019. In this respect, the following information is available: (i) Cash book showed an overdrawn balance of Rs. 3,928,000. (ii) Cheques outstanding as at 30 June 2019 amounting to Rs. 1,250,000 included: a cheque of Rs. 10,000 dated 8 December 2018 issued to a welfare organization for donation. a cheque of Rs. 150,000 dated 20 June 2019 mailed to a supplier on 10 July 2019. (iii) A cheque of Rs. 391,000 issued to a supplier was recorded in the cash book as Rs. 319,000. (iv) (Cheques received from customers amounting to Rs. 670,000 were recorded in the cash book but not credited in bank statement. These cheques included a cheque dated 10 July 2019 amounting to Rs. 25,000 received from a customer on 28 June 2019. (v) A bank debit advice dated 30 June 2019 for interest charges amounting to Rs. 80,000 was received in July 2019. Required: (a) Compute the corrected cash book balance as at 30 June 2019. (04) (b) Compute the bank balance as would be appearing in the bank statement as at 30 June 2019. (04) Latest update: April 2020 CAF 1 – Bank Reconciliation Statement ANSWER 01 Particulars Balance as per cash book (adjusted) Un-presented cheques [70,000 + 90,000 + 100,000] Un-credited cheques Balance as per bank statement Total Ref. Dr. (Rs) 1,500,000 260,000 Cr. (Rs) 210,000 1,550,000 1,760,000 1,760,000 ANSWER 02 b/d Under-casting debit side (a) c/d Cash Book (Bank column) 1,660,000 Error (b) 4,275,000 – 2,475,000 200,000 Dishonoured cheque (c) Bank charges (d) 344,000 2,204,000 Particulars Balance as per cash book (adjusted) Un-presented cheques Un-credited cheques Balance as per bank statement Total Ref. Dr. (Rs) (e) (e) 520,000 2,204,000 Cr. (Rs) 344,000 626,000 450,000 970,000 ANSWER 970,000 03 CONNOLLY Bank Reconciliation Statement (As at xx-xx-xxx) Particulars Ref Dr. (Rs ‘000) Balance as per cash book β 5,100 Un-presented cheques 18,500 Un-credited cheques Balance as per bank statement Total 23,600 b/d 1,800,000 220,000 184,000 Connolly Cash Book (Bank column) 5,350 Bank charges c/d 5,350 © kashifadeel.com Cr. (Rs ‘000) 16,200 7,400 23,600 250 5,100 5,350 Page | 13 CAF 1 – Bank Reconciliation Statement ANSWER Page | 14 04 AL-MURTAZA COMPANY Bank Reconciliation Statement As at August 31, 2013 Particulars Ref Balance as per cash book W1 Un-presented cheques [c] 670 679 690 996 997 999 Un-credited amounts [d] (83,250 + 144,641) Balance as per bank statement (b) Total Dr. (Rs) 369,206 13,353 14,152 17,108 3,535 14,430 23,629 455,413 W1 – Al-Murtaza Company Cash Book (Bank column) b/d (a) 272,178 Payment (e)(ii) Revenue (e)(i) 30,000 Overcasting (e)(iii) 4,800 Receivables (e)(iv) 87,188 c/d 394,166 ANSWER Cr. (Rs) 227,891 227,522 455,413 24,960 369,206 394,166 05 ABC TEXTILES Bank Reconciliation Statement As at December 31, 2013 Particulars Ref Dr. (Rs) Balance as per cash book W1 Un-presented cheques 377,784 – 5,000 (ii), (vii) 372,784 Un-credited cheques (iv) (v) Error by bank 13,200 x 2 times (xii) 26,400 Balance as per bank statement (i) 806,436 Total 1,205,620 W1 – ABC Textiles Cash Book (Bank column) Mark-up (iii) 118,686 b/d β Time barred cheque (vii) 5,000 Discount allowed (viii) Recording error 7,500 x 2 times (ix) 15,000 Error (125,000 – 12,500) (xi) c/d 758,520 Magazine subscription (vi) 897,206 Cr. (Rs) 758,520 250,600 196,500 1,205,620 771,062 10,500 112,500 3,144 897,206 In point (x) the time barred cheque is an event after the relevant period. The cheque will be considered cancelled when it will become time-barred. Latest update: April 2020 CAF 1 – Bank Reconciliation Statement ANSWER 06 MUBARAK & COMPANY Bank Reconciliation Statement As at December 31, 2013 Ref Dr. (Rs) Particulars Balance as per cash book β Un-presented cheques Un-credited cheques Balance as per bank statement Total (ix) (i) given Cr. (Rs) 50,500 467,200 467,200 49,200 367,500 467,200 W1 – ABC Textiles Cash Book (Bank column) Mr. Mubarak (wrong deposit) (v) 10,000 b/d β Receivables (vi) 49,900 Bank charges (ii) Receivables (cheque returned) (iii) Dividend (xi) 12,000 Mr. Bilal (recording error) (xii) 9,000 Annual subscription (iv) Vendor (2,600 x 3 (vii)) Mr. Bashir (entered twice) (viii) c/d 50,500 Discount allowed (x) 131,400 Journal entries Bank charges (ii) 1 Bank 79,800 1,700 4,200 1,000 7,800 36,400 500 131,400 1,700 1,700 (iii) 2 Receivables Bank 4,200 (iv) 3 Annual subscription Bank 1,000 (v) 4 Bank 10,000 (vi) 5 (vii) 6 Hire purchase vendor Bank 7,800 (viii) 7 Mr. Bashir Bank 36,400 (x) 8 Discount allowed Bank (xi) 9 (xii) 10 4,200 1,000 Mr. Mubarak 10,000 Bank 49,900 Receivables 49,900 7,800 36,400 500 500 Bank 12,000 Dividend 12,000 Bank 9,000 Mr. Bilal 9,000 Corrected cash book (bank column) balance: (79,800) + 80,900 – 51,600 = (50,500) © kashifadeel.com Page | 15 CAF 1 – Bank Reconciliation Statement ANSWER Page | 16 Wrong side recording error 1,550,000 x 2 (i) Cheque issued error 4,005,000 – 4,050,000 (iii) Time barred cheque (iv) Twice recorded (v) Balance c/d 07 Ranjha Enterprises Bank Book Balance b/d 3,100,000 Dishonored cheque (i) 45,000 125,000 50,000 630,000 3,950,000 Ranjha Enterprise Bank Reconciliation Statement as at 30 June 2015 Particulars Dr. Rs. Balance as per cash book Un-credited cheques 1,550,000 – 500,000 dishonored (i) Bank error (charges wrongly recorded) 750,000 – 510,000 (ii) Bank error 4,005,000 – 4,500,000 (iii) Balance as per bank statement (overdrawn) 2,415,000 TOTAL 2,415,000 ANSWER 3,450,000 500,000 3,950,000 Cr. Rs. 630,000 1,050,000 240,000 495,000 2,415,000 08 Part (a) Galaxy Enterprises Corrected bank book balance Bank Book b/d 856,000 Dishonoured cheque Reversal of time barred cheque Reversal of post-dated cheque 250,000 Reversal cheque incorrect name 455,000 Bank charges Correction in customer cheque 9,000 Subscription charges c/d 1,570,000 Correction journal entries for the month of January 2016 Date Description 2016 31-Jan Bank Accounts payable Reversal of time barred cheque # 111 31-Jan Bank Accounts payable Reversal of cheque # 666 issued with an incorrect name 31-Jan Accounts receivable Bank Reversal of dishonored cheque # 1XX 31-Jan Accounts receivable Bank Reversal of post-dated cheque of 1 March 2016 mistakenly presented to the bank in De. 2015 Latest update: April 2020 140,000 135,000 8,500 120,000 1,166,500 1,570,000 Debit Credit -------Rupees------250,000 250,000 455,000 455,000 140,000 140,000 135,000 135,000 CAF 1 – Bank Reconciliation Statement 31-Jan Bank 31-Jan Receivable Correction of a customer’s cheque of Rs. 54,000 mistakenly recorded as Rs. 45,000 Bank charges Subscription charges Bank To record bank charges and annual subscription paid 9,000 9,000 8,500 120,000 128,500 Part (b) Bank reconciliation statement for the month of January 2016 Corrected bank book balance Less: Cheques issued but not presented for payments: 444 777 Various Add: Cheques deposited into the bank but not yet cleared 2XX 3XX Various Balance as per bank statement Dr Rs. 1,166,500 Cr Rs. 79,000 500,000 1,350,000 3,095,500 ANSWER 70,000 63,000 1,780,000 1,182,500 3,095,500 09 Part (a) Eden Garments Date 30-06 Description Balance b/d (i) (i) (iii) Account payable Repair charges Account receivable (iv) Dividend income Bank account Rupees Date Description (i) Account payable 760,000 ( 85,000-58,000) 50,000 (ii) Account receivable 4,630 (ii) Discount expense (76,000 354,000 / 0.95) - 76,000 (iv) Bank charges 50,000 (7,850-1,250) (iv) Subscription charges 30-06 Balance c/f 1,218,630 © kashifadeel.com Rupees 27,000 366,000 4,000 6,600 12,000 803,030 1,218,630 Page | 17 CAF 1 – Bank Reconciliation Statement Part (b) Page | 18 Balance as per bank book Cheques issued by EG but not yet paid by the bank: As given in question paper Cheque returned from the bank now recorded Misplaced cheque now reversed Dr. Rs. 803,030 Cr. Rs. 3,856,300 (50,000) (4,630) 3,801,670 Cheques deposited but not credited by the bank: As given in question paper Cheque deposited and returned by the bank now recorded Bank charges over charged Unidentified difference (balancing) Balance as per bank statement – overdraft 6,460,000 (366,000) 6,094,000 1,250 300 (1,490,850) 6,095,550 6,095,550 ANSWER 10 Part (a) b/d Payables (i) Suspense (iv) [4,598,000 – 4,589,000] Cash Book (Bank column) 2,845,390 Payables [37,250 – 32,750 (i)] 9,650 Receivables (ii) Bank charges [9,240 – 2,500 (iii) 9,000 c/d 2,864,040 4,500 35,000 6,740 2,817,800 2,864,040 Part (b) Bank Reconciliation Statement For the month February 2017 Particulars Ref. Balance as per cash book (adjusted) Un-presented 869,200 given + [37,250 – 32,750 (i)] – 9,650 outdated (i) Dr. (Rs) 2,817,800 Cr. (Rs) 864,050 Un-cleared 456,350 given – 35,000 reversal of post-dated cheque (ii) 421,350 Error by bank / Bank charges (iii) 2,500 Balance as per bank statement Total 3,681,850 ANSWER 3,258,000 3,681,850 11 SANDFORD Bank Reconciliation Statement (As at xx-xx-xxx) Particulars Ref Dr. (Rs ‘000) Balance as per cash book W1 750 Un-presented cheques 4,700 Un-credited cheques Balance as per bank statement β 2,750 Total 8,200 Latest update: April 2020 Cr. (Rs ‘000) 8,200 8,200 CAF 1 – Bank Reconciliation Statement b/d W1 - SANDFORD Cash Book (Bank column) 1,600 Bank charges Direct debit Dishonored cheque c/d 1,600 150 400 300 750 1,600 Page | 19 ANSWER 12 Part (a) Possible causes of disagreements between the bank balance shown in the bank statement and the bank book balance include: (i) Uncredited lodgement / Cheque deposited but not cleared (ii) Unpresented cheques (iii) Bank charges/interest (iv) Posting errors (v) Casting errors (vi) Direct credit (vii) E-payment (viii) Automated teller machine (ATM) withdrawal (ix) Standing order (x) Credit/Debit transfer (xi) Dishonoured cheques Part (b) Adjusted Bank book as at 31 December 2014 Bank Book b/d 34,000 e-payment charges Overcast – bank book Undercast- bank book Wrong posting (65,000 x 2) e-payment to supplier Cheque entered twice Wrong posting of dividend c/d 1,092,000 Subscription fees 1,126,000 Bank Reconciliation Statement as at 31 December 2014 Particulars Dr. Rs. Balance as per cash book Un-credited cheques Bank error (interest on bank deposit not yet posted by bank) Bank error (over-posting of cheque drawn) 300,000 – 30,000 Unpresented cheques 325,000 Balance as per bank statement (overdrawn) 1,712,000 TOTAL 2,037,000 © kashifadeel.com 35,000 90,000 42,000 130,000 720,000 80,000 9,000 20,000 1,126,000 Cr. Rs. 1,092,000 630,000 45,000 270,000 2,037,000 CAF 1 – Bank Reconciliation Statement ANSWER Page | 20 13 Bank Book (Bank column of Cash Book) b/d 441,500 Error in op balance 133,500 x 2 X10 Chq 352,000 – 325,000 27,000 Standing order Direct transfer 38,000 Dishonored cheque Bank charges c/d (Corrected Balance) 506,500 Bank Reconciliation Statement As on February 2018 Particulars Ref. Balance as per cash book (Corrected) Un-presented Cheques X06 X11 Un-cleared items 25 Feb 26 Feb Error by bank Balance as per bank statement Total Dr. (Rs) 20,000 150,000 622,000 0 792,000 ANSWER 267,000 15,000 200,000 4,500 20,000 506,500 Cr. (Rs) 182,000 294,000 0 316,000 792,000 14 Part (a) Lamda Establishment Description Donation expense A/c payables Balance c/d Bank in cash book Rupees Description 10,000 Balance b/d 150,000 A/c payables (391,000 – 319,000) A/c receivables 3,945,000 Interest charges 4,105,000 Rupees 3,928,000 72,000 25,000 80,000 4,105,000 Part (b) Bank balance as per the bank statement Bank Reconciliation Statement as at 30 June 2019 Balance as per cash book Unpresented cheques 1,250,000 – 10,000 time barred – 150,000 cheque issued later Uncleared cheques 670,000 – 25,000 post dated Balance as per the bank statement - Overdraft Latest update: April 2020 Debit Rupees Credit Rupees 3,945,000 1,090,000 645,000 3,500,000 4,590,000 4,590,000 CAF 1 – Bank Reconciliation Statement ICAP OBJECTIVE BASED QUESTIONS 01. The following bank reconciliation statement has been prepared by a business. Bank reconciliation statement as at April 30, 2018 Rs. Balance as per bank statement (Cr) 45,200 Add: Outstanding cheques 11,500 Less: Uncleared lodgements 13,100 Balance as per cash book (Dr) 43,600 Assuming that all items other than balance as per cash book is correct; what is the correct balance as per cash book? (a) Rs.43,600 Dr as per statement in question (b) Rs.43,600 Cr (c) Rs.46,800 Dr (d) Rs.46,800 Cr 02. Debit balance of Rs.5,000 as per bank statement means: (a) Rs.5,000 payable to business by the bank (b) Rs.5,000 receivable from business by the bank (c) Rs.5,000 deposited by the business during the month (d) Rs.5,000 withdrawn from the bank by business during the year 03. The following bank reconciliation statement has been prepared by a trainee accountant: Rs. Overdraft as per bank statement 6,980 Less: Outstanding cheques 10,460 3,480 Add: Deposits credited after date 11,800 Cash at bank as per cash book 15,280 What should be the correct balance as per cash book? (a) Rs.15,280 balance at bank as stated (b) Rs.5,640 balance at bank (c) Rs.15,280 overdrawn (d) Rs.5,640 overdrawn 04. At the end of 31 March 2019, balance as per cash book of Imtiaz is Rs.10,200 (Dr) which did not agree with the balance as per the bank statement. On investigation following information was identified; A standing order of Rs.350 was paid by the bank did not appear in the cash book. Dividend received directly in the bank was Rs.30 Bank credited interest for the quarter Rs.350; it was included in cash book as Rs.530 A customer cheque deposited in the bank Rs.120 was dishonoured What is the corrected balance as per cash book? (a) Rs.10,170 Dr (b) Rs.10,170 Cr (c) 9,580 Dr (d) 9,580 Cr © kashifadeel.com Page | 21 CAF 1 – Bank Reconciliation Statement 05. Page | 22 A business identified that there is a difference between balance of cash book and the balance as per bank statement at end of 28 February 2019. On investigation it was revealed that: Bank debits account of business for bank charges Rs.30 and standing order Rs.150. Bank erroneously debits bank account of business for a cheque of Rs.40. Business has credited the bank account for quarterly interest income Rs.150. What is the total amount of adjustment to be made in cash book of business? (a) Rs.180 Cr and Rs.150 Dr (b) Rs.180 Cr and Rs.300 Dr (c) Rs.220 Cr and Rs.300 Dr (d) Rs.220 Dr and Rs.300 Cr 06. Balance of bank account as per cash book is Rs.35,000 (Dr) while balance as per bank statement is Rs.32,500 (Cr). Difference is explained as Uncleared lodgments of Rs.2,500 not included in the bank statement. What is the amount of bank balance to be reported in Statement of financial Position? (a) Rs.35,000 Cash at bank (b) Rs.35,000 Overdraft (c) Rs.32,500 Cash at bank (d) Rs.32,500 Overdraft 07. A business is in process of reconciling its cash book with banks statement. Which of the following item require entry in cash book? (a) Bank service charges (b) Deposits credited by the bank after the date of the bank statement (c) Cheque of another account erroneously credited by bank (d) Cheques presented by suppliers after the date of bank statement 08. A business is in process of preparing its bank reconciliation statement. The balance of cash book did not agree with the balance in bank statement. The following information is available: Balance as per cash book before comparing bank statement Rs. 11,000 (Dr) Outstanding Cheques Rs.1,550 Outstanding lodgments Rs.1,200 Bank charges Rs.50 Bank interest income Rs.100 What is the balance as per bank statement? (a) Rs.11,200 Dr (b) Rs.11,400 Dr (c) Rs.11,400 Cr (d) Rs.11,200 Cr 09. A business received a bank statement showing a credit balance of Rs.7,400. On investigation its accountant discovered that the bank statement does not show cheques received from customers Rs.16,200 and banked and same for cheque payments to suppliers Rs.18,500. The bank statement also shows bank charges of Rs.250 which has not yet been recorded in ledger. What is the current balance as per cash book? (a) Rs.5,350 Cr (b) Rs.5,350 Dr (c) Rs.5,100 Dr (d) Rs.5,100 Cr Latest update: April 2020 CAF 1 – Bank Reconciliation Statement 10. Following information has been collected from the books of Murtaza as at 31 January 2019: Balance as per cash book Rs.15,000 (Dr) On scrutiny of bank statement it was found: Unpresented Cheques Rs.2,500 Uncredited lodgements Rs.1,500 Bank charges Rs.200 Bank debits Muratza for bank interest Rs.120 instead of Rs.150. No amount was recorded in cash book of Murtaza Further it was found that: Receipt of Rs.1,500 was recorded on credit side of cash book Payment of Rs.1,200 was recorded on debit side of cash book 11. What is the corrected cash book balance of Murtaza? (a) Rs.15,370 Dr (b) Rs.15,250 Dr (c) Rs.15,250 Cr (d) Rs.15,370 Cr A bank statement shows a balance of Rs.4,000 in credit. On examining the bank statement, it was found that the cheques of Rs.600 deposited in bank as per the cash book not yet on the bank statement and cheques of Rs.1,000 issued out but not yet appeared on the bank statement. Furthermore, the cash book shows deposit interest received of Rs.100 but this is not yet on the statement. What is the balance as per cash book? (a) Rs.3,700 (b) Rs.4,500 (c) Rs.5,000 (d) Rs.3,900 12. If it was found that the receipt side of the cash book has been under-casted, then in preparing bank reconciliation statement, it should be: (a) Deducted from balance as per cash book (b) Added in balance as per bank statement (c) Added in balance as per cash book (d) Deducted from balance as per bank statement 13. Which of the following statements is correct? (a) Credit balance as per bank statement means a bank overdraft (b) Debit balance as per bank statement means a bank overdraft (c) Debit balance as per cash book means a bank overdraft (d) Credit balance as per cash book means an asset 14. Which of the following require deduction from cash book balance while preparing bank reconciliation statement? (a) Direct deposit by a customer into bank but entered in cash book (b) Standing orders paid by the bank not yet entered in cash book (c) Unpresented cheques not yet paid by bank (d) Bank debits interest Rs. 2,500 instead of Rs. 5,200 © kashifadeel.com Page | 23 CAF 1 – Bank Reconciliation Statement 15. Page | 24 The following information relates to bank reconciliation: (i) The bank balance in the cash book before taking the items below into account was Rs.9,870 overdrawn (ii) Bank charges of Rs.750 on the bank statement have not been entered in the cash book (iii) The bank has credited the account in error with Rs.645 which belongs to another customer (iv) Cheque payments totaling Rs.4,385 have been entered in the cash book but have not been presented by payment (v) Cheques totaling Rs.6,500 have been correctly entered on the debit side of the cash book but have not been paid in at the bank What was the balance as shown by the bank statement? (a) Rs.10,970 overdrawn (b) Rs.12,200 overdrawn (c) Rs.12,090 overdrawn (d) Rs.11,550 overdrawn 16. Balance as per bank statement of Asim was Rs.11,600 credit as on April 30, 2018 which was not in agreement with the balance as per cash book. On investigation the following items were detected: Cheques issued and paid by the bank for Rs.5,500 but recorded in the cash book as Rs.500 Bank service charges not entered in the cash book Rs.420 Outstanding lodgements Rs.1,300 Bank has erroneously debited a cheque of Rs.900 to Asim actually the cheque was issued by Asif. Unpresented cheques Rs.1,200 What should be the balance as per cash book before adjustments? Rs. ___________ 17. Following information is available regarding cash at bank of a business: Cash at bank as per bank column of the cash book Rs.4,910 Unpresented cheques Rs.630 Cheques received & paid into the bank, but not yet entered on the bank statement Rs.460 Credit transfers entered on the bank statement but not entered in the cash book Rs.340 What is Cash at bank as per bank statement? Rs. ___________ 18. The bank column of a cash book showed a credit balance of Rs.8,000. There were unpresented cheques amounting to Rs.2,500. The bank statement showed bank charges, Rs.900, which were not recorded in the cash book. What is the balance on the bank statement? Rs. ___________ 19. When preparing a bank reconciliation statement the following information is available. Balance as per cash book Rs.25,000 (Dr) Outstanding cheques Rs.1,500 uncleared lodgements 1,300 Standing order shown on the bank statement (not appearing in a cash book) Rs.200 Dividend directly deposited in the bank (not appearing in the cash book) Rs.25 What is the balance as per bank statement? Rs. ___________ Latest update: April 2020 CAF 1 – Bank Reconciliation Statement 20. Balance as per bank statement was Rs.1,000 in debit. Comparison of bank statement with cash book revealed that cheques of Rs.3,200 paid in per the cash book but not yet on the bank statement and cheques of Rs.500 paid out but not yet appeared on the bank statement. In addition the bank statement shows direct deposit of Rs.800 by a customer but it is not recorded in cash book. What is the balance as per cash book after adjustments? Rs. ___________ 21. The main purpose of preparing a bank reconciliation statement is? (a) To know the bank balance (b) To know the balance of bank statement (c) To correct the cash book (d) To identify causes of difference between cash book and bank statement 22. Bank Reconciliation Statement is prepared by (a) Bank (b) Accountant (c) Customer (d) Auditors 23. Bank reconciliation statement is (a) Part of bank statement (b) Part of the cash book (c) A separate statement (d) A sub-division of journal 24. Favorable balance means? (a) Credit balance in the cash book (b) Credit balance in Bank statement (c) Debit balance in cash book (d) Both b and c 25. Unfavorable balance means? (a) Credit balance in the cash book (b) Credit balance in Bank statement (c) Debit balance in cash book (d) Debit balance in petty cash book 26. When cheque is not paid by the bank, it is called? (a) Stale cheque (b) Dishonored cheque (c) Bearer cheque (d) None of the above 27. Which of the following would not affect bank reconciliation? (a) Dishonored cheque (b) Bank interest (c) Discount received (d) Unpresented cheque 28. An amount of Rs. 1,000 is debited twice in the bank statement. When overdraft as per the cash book is the starting point? (a) Rs. 1,000 will be added (b) Rs. 1,000 will be deducted (c) Rs. 2,000 will be deducted (d) Rs. 2,000 will be added © kashifadeel.com Page | 25 CAF 1 – Bank Reconciliation Statement 29. Bank sent debit advice of Rs. 50,000 to company being interest on overdraft. It was not entered in cash book. Identify the correct adjustment in cash book? (a) Rs. 50,000 will be debited (b) Rs. 50,000 will be credited (c) No adjustment (d) Rs. 100,000 will be subtracted 30. A discount of Rs. 20,000 was given to a customer on his prompt repayment of debt but the cashier entered the gross amount in cash book. Page | 26 What should be the adjustment in cash to work out the correct balance of cash book? (a) Rs. 20,000 will be debited in cash book (b) Rs. 20,000 will be credited in cash book (c) Rs. 40,000 will be debited in cash book (d) Rs. 40,000 will be credited in the cash book 31. In the Bank reconciliation statement “Deposit in transit” is usually: (a) Subtracted from bank statement balance (b) Added to bank statement balance (c) Added to Cash book balance (d) Subtracted from cash book balance 32. Interest credited to bank account (a) Add to cash book balance (b) Deduct from cash book balance (c) Add to bank statement balance (d) Deduct from bank statement balance 33. Bank inadvertently charged your bank account for another company's bank fees (a) Add to cash book balance (b) Deduct from cash book balance (c) Add to bank statement balance (d) Deduct from bank statement balance 34. A company had a receipt of Rs.989,000 and correctly prepared its bank deposit slip for Rs.989,000. However, the company recorded the receipt in its Cash account as Rs.998,000. How is the difference of Rs.9,000 handled on the bank reconciliation? (a) Add to cash book balance (b) Deduct from cash book balance (c) Add to bank statement balance (d) Deduct from bank statement balance Latest update: April 2020 CAF 1 – Bank Reconciliation Statement OBJECTIVE BASED ANSWERS 01. (c) 02. (b) 03. (d) 04. 05. (c) (b) 06. (a) 07. 08. (a) (c) Uncleared lodgments are added and outstanding cheques are deducted from balance as per bank statement. Rs. 45,200 – 11,500 + 13,100 = Rs. 46,800 (Normal debit balance) Dr balance as per bank statement means credit balance as per cash book i.e. a liability of business and asset of bank. The balance in bank statement should be taken as negative. = – Rs. 6,980 – 10,460+11,800= – Rs. 5,640 overdraft (negative balance) = Rs. 10,200 – 350+30 [– 530+350] – 120= Rs. 9,580 debit Rs. 180 Cr (bank charges and standing order payment) and Rs. 300 Dr (150 x 2) the interest should have been debited (not credited) in cash book Uncleared lodgments are reconciling item cash book balance is not adjusted for those. Balance to be reported in the statement of financial position is balance as per cash book. All other items belong to reconciliation statement Balance as per cash book adj. Uncredited lodgment Unpresented cheques Balance as per bank statement Dr Rs. 11,050 1,550 12,600 Particulars As per question Interest income 09. Cr. Rs. 1,200 11,400 12,600 Cash book Rs. Particulars 11,000 Bank charges 100 c/d Rs. 50 11,050 11,100 11,100 (b) Dr Rs. Balance as per bank statement Uncredited lodgment Unpresented cheques Balance as per cash book adjusted Particulars Unadjusted bal β 18,500 5,100 23,600 Cash book Rs. Particulars 5,350 Bank charges c/d 5,350 © kashifadeel.com Cr. Rs. 7,400 16,200 23,600 Rs. 250 5,100 5,350 Page | 27 CAF 1 – Bank Reconciliation Statement 10. (b) Cash book Particulars As per question Wrongly recorded 1,500x2 Page | 28 Rs. 15,000 3,000 Particulars Bank interest Payment wrongly recorded 1,200 x 2 Bank charges c/d 18,000 11. 200 15,250 18,000 (a) Dr Rs. Balance as per bank statement Outstanding lodgment Interest not appearing in bank statement Unpresented cheques Cash book balance after adjustments 12. (c) 13. (b) 14. (b) 15. (c) 100 1,000 3,700 4,600 Cr. Rs. 4,000 600 4,600 Errors in cash book are adjusted to the balance as per cash book and undercasting of error would have decreased balance of cash that needs to be increased now. Debit balance as per bank statement means business is a debtor of bank, hence, bank overdraft. Standing order and bank charges both are payments and would be deducted from cash book balance. Dr Rs. Balance as per cash book adj. Uncredited lodgment Outstanding cheques Bank error Balance as per bank statement 4,385 645 12,090 17,120 Cash book Rs. Particulars b/d as per question 10,620 Bank charges 10,620 Particulars c/d 16. Rs. 150 2,400 Cr. Rs. 10,620 6,500 17,120 Rs. 9,870 750 10,620 Rs. 18,020 Dr Rs. Balance as per bank statement Outstanding lodgment Cheque erroneously debited Unpresented cheques Cash book balance after adjustments Particulars Unadjusted bal β 1,200 12,600 13,800 Cash book Rs. Particulars 18,020 Error in cheque Bank charges c/d 18,020 Latest update: April 2020 Cr. Rs. 11,600 1,300 900 13,800 Rs. 5,000 420 12,600 18,020 CAF 1 – Bank Reconciliation Statement 17. Rs. 5,420 Balance as per cash book adj. Uncredited lodgment Unpresented cheques Balance as per bank statement Dr Rs. 5,250 460 630 5,880 Particulars As per question Credit transfer 18. 5,250 5,250 5,250 Rs. Rs. 6,400 Balance as per cash book adj. Unpresented cheques Balance as per bank statement Particulars c/d 2,500 6,400 8,900 8,900 Rs. 8,000 900 8,900 8,900 Rs. 25,025 Dr Rs. 24,825 Particulars As per question Dividend Cr. Rs. 1,300 1,500 26,325 25,025 26,325 Cash book Rs. Particulars 25,000 Standing order 25 c/d Rs. 200 24,820 25,025 25,025 Rs. 1,700 Dr Balance as per bank statement Uncredited lodgment Unpresented cheques Balance as per cash book adjusted 21. 22. 23. Cr. Rs. 8,900 Cash book Rs. Particulars b/d as per question 8,900 Bank charges Balance as per cash book adj. Uncredited lodgment Outstanding cheques Balance as per bank statement 20. 5,420 5,880 Cash book Rs. Particulars 4,910 340 c/d Dr Rs. 19. Cr. Rs. (d) (b) (c) © kashifadeel.com Dr Rs. 1,000 Cr. Rs. 3,200 500 1,700 3,200 3,200 Page | 29 CAF 1 – Bank Reconciliation Statement Page | 30 24. 25. 26. 27. 28. 29. 30. 31. 32. 33. 34. (d) (a) (b) (c) (a) (b) (b) (b) (a) (c) (b) Latest update: April 2020