Salary Sacrifice

advertisement

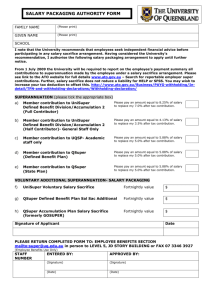

Salary Sacrifice Introduction to tax-efficient work-related benefits What is Salary Sacrifice and when is it advantageous? A salary sacrifice occurs when an employee agrees to give up part of the cash remuneration due under their contract of employment (i.e. part of their salary) in return for the employer agreeing to provide some sort of non-cash benefit. When the non-cash benefit can be provided tax-free, there is an overall saving to the employee. In some cases, the employer also benefits through reductions in liability for national insurance on the sacrificed portion of the employee’s salary. There is no point in making a salary sacrifice if the benefit provided would itself be taxable. Salary sacrifice schemes at Imperial College The College offers salary sacrifice for the following: (i) (ii) (iii) (iv) (v) (vi) Pension membership of USS or SAUL (but not the NHS Pension Scheme), under a scheme known as PensionSMART Workplace nurseries, i.e. the Early Years Education Centre (EYEC) and nurseries at Hammersmith and Charing Cross Hospitals. Childcare vouchers provided through Computershare Voucher Services Car Parking Tuition fees for the Executive MBA at Imperial College. For donations in support of the College’s programme of providing additional bursaries and scholarships for future students The College does not operate the Cycle2Work scheme since the tax benefits are considered marginal, and the administration unduly complex. Instead, employees are offered interest-free loans to facilitate purchase of bicycles. See http://www.imperial.ac.uk/sport/get-active/cycling-at-imperial/staff-cycling/ Students and Casual Workers Salary sacrifice does not work for student bursaries (because there is no tax to pay, and hence no saving to be made) or casual earnings (because there is no contractually guaranteed salary which could be sacrificed). How is a salary sacrifice put into effect? In every case, a salary sacrifice is constituted by means of a mutually-agreed variation in the employment contract. The way this is achieved depends upon the scheme: (i) (ii) (iii) (iv) (v) Sacrifice for pensions (USS or SAUL) is made automatically at the time the employee accepts an offer of employment from the College. The employee may opt out of the salary sacrifice within three months of joining, and thereafter annually on 1 December, by sending the appropriate form to the pensions office. Full details are provided on the PensionSMART web-page Childcare vouchers through Computershare must be applied for electronically over the web. For Workplace nurseries (EYEC or nurseries at Hammersmith and Charing Cross Hospitals), parents should contact Margaret Kennedy, 8 Princes Gardens, SW7 1NA (020 7594 5121) who will supply the application form and arrange for a revision to the employment contract to be issued. Car parking is managed by the Facilities Management Division, and the sacrifice is effected by an exchange of emails. Tuition fees for the Executive MBA programme in the College’s Business School are effected by individually-tailored arrangements. Basic conditions Salary sacrifice cannot and does not refer to past earnings, and constitutes a change in the terms and conditions of employment with the College. The agreement must be signed before the end of the month preceding that in which the employee wishes the sacrifice to take effect. During the agreed period, no rights in relation to the sacrificed portion of salary can be exercised, and the agreement cannot be revoked or changed retroactively in any way. The following conditions must be fulfilled: The agreement must be made in advance to ensure that the relevant remuneration is sacrificed before the employee has earned it (in accordance with HMRC regulations). The election must be for a defined monetary amount (a fixed sum or a percentage of salary). The tax savings The effect of salary sacrifice is top remove the top slice of your income from the tax net. The exact amount you will save depends upon how much of your income falls into each tax band. General principles: (i) (ii) The more you earn, the more you will save by salary sacrifice If you don’t pay any tax, there’s nothing to save, and no point in entering into a salary sacrifice arrangement. The tax rates, annual allowances and tax bands vary from year to year, and the exact rates can be found on the HMRC web-site, here: https://www.gov.uk/government/collections/rates-and-allowances-hm-revenue-andcustoms However, to a reasonable approximation, the rates are as follows: Slice of annual income The bottom slice of your annual income, i.e. that falling below £10,000 The next slice, between £10,000 and £42,000 Above £42,000 Above £150,000 Income tax rate Nil National insurance Nil Combined rate Nil 20% 12% 32% 40% 45% 2% 2% 42% 47% You can calculate roughly how much you save by entering into a salary sacrifice as follows:(i) (ii) (iii) (iv) (v) Find out your annual salary before any salary sacrifice. This will be your monthly gross salary, which can be found on your pay slips, multiplied by twelve. Add up the annual value of any existing salary sacrifice, and any new ones proposed. If the sacrifice period is less than a year, use the monthly amount and multiply by 12 to produce an annualised figure. Work out how much of the annual salary sacrifice figure (or the combined figure, if you are in several different schemes) falls into the income slices from the table above. The annual saving is the amount of the sacrifice multiplied by the combined percentage rate shown in the table above. If the sacrifice period is less than a year, divide the annual saving by 12 to estimate the monthly saving for the duration of your membership of the scheme. Complications: The actual calculation of the savings is slightly more complex than suggested above, because:(i) (ii) (iii) (iv) tax and NIC thresholds are not precisely aligned (see HMRC web-site); some people’s tax-free personal allowances do not match the standard figure, for example if they are also making charitable donations through gift aid; for people earning over £100,000, the personal allowance is reduced by £1 for every extra £2 earned, until it is wiped out completely at around £120,000. [Note; the effect of salary sacrifice is particularly advantageous if you happen to fall into this range, because your effective marginal rate of tax is about 60% - so the savings are particularly worthwhile.] some people have income from other sources, for example dividends, interest or outside earnings, which increase their total income, and hence (v) (vi) increases the upper limit of the top slice. [This usually makes salary sacrifice more attractive, not less so.] Some people have deductible expenses, which reduces the top slice. Until April 2016, employees who are members of any of the College pension schemes enjoy a small rebate (1.4%) on their national insurance, so the savings from salary sacrifice are slightly less good. In addition to the employee savings, the College makes savings of employer’s NICs. These savings are not available to individual employees, but will be used to improve facilities and meet the costs of running the salary sacrifice schemes. Other Implications of a Salary Sacrifice Scheme When entering a salary sacrifice arrangement, it is important for the employee to consider the possible effect that a reduction in their contractual salary might have on: Their future right to the original (higher) cash salary. Future mortgage applications. Life insurance multiples. Any pension scheme being contributed to (see FAQ 7, below). Entitlement to Working Tax Credit or Child Tax Credit. (see FAQ19) Entitlement to State Pension or other benefits such as Statutory Maternity Pay (see FAQ 9). More information about the implications of a salary sacrifice scheme can be found on the HMRC Website: http://www.inlandrevenue.gov.uk/specialist/salary_sacrifice.pdf Frequently Asked Questions The following matters relate to salary sacrifice in general. There may be additional questions relating to the individual schemes listed above, which are explained on their web-page. Q1: Can anyone apply for salary sacrifice? No, only those who are employed by the College may do so. Salary sacrifice does not work for students or guests. Q2: Is there a minimum or maximum time period for which I may sacrifice salary? It is College policy only to allow salary sacrifice for complete months beginning on the 1st of the month, and for a minimum of three months. [Note: salary sacrifice for pensions takes effect immediately from the date you join the College or the pension scheme.] There is no maximum period for salary sacrifice. Q3: Is there any maximum to the amount I may sacrifice from my salary? The total amount sacrificed from any given month’s salary must not be so great as to cause:(i) (ii) Your earnings to fall below the National Minimum Wage (i.e. after all sacrificed amounts have been deducted). This situation is only likely to arise if the monthly sacrifice is very large, or your working hours are very few. The payroll office will look at individual cases at risk. Information on the NMW can be found here: https://www.gov.uk/national-minimum-wagerates Your net pay, after all deductions, to fall below zero. This is only likely to arise if you have exceptionally large deductions, for example a large season ticket loan needing to be repaid. In addition, childcare vouchers are limited to an annual amount which is dependent upon the employee’s highest tax rate. Further details are provided in the childcare vouchers page. Q4: What if I want to withdraw from a salary sacrifice arrangement? If the sacrifice was for a fixed time period, you may only leave the scheme at the end of the agreed sacrifice period. The College will continue to make available whatever benefits you opted to receive, regardless of whether you are able to utilise them. If you have an open-ended salary sacrifice you should give notice of your wish to withdraw at the earliest opportunity, and the College will normally accede to your request with effect from the first day of the month following that in which you made your request. Please note, however, that there is no automatic right to revert to your original salary. This requires both the employer and employee to agree to the change. Back-dated withdrawals from salary sacrifice are only permitted in very exceptional circumstances, such as manifest administrative error. Q5: What if my needs change? (e.g. the benefit required is reduced or increased in scale, such as from a part-time to a full-time nursery place)? First contact the administrator of the relevant scheme. If agreed, a supplemental variation to your employment contract can be issued. Q6 Will I always be able to use the Salary Sacrifice Scheme whilst I am employed by the College? Yes, as long as the relevant scheme continues in force, and providing that you continue to receive a salary sufficiently large to enable you to make an appropriate sacrifice. (See also Q3 and Q20.) Q7: Will I lose any university pension benefits by taking an abated salary? If you are a member of USS or SAUL your pension contributions (employer’s and employee’s) will be maintained at their normal (pre-sacrifice) level, and you will continue to be entitled to the normal benefits of these schemes. By contrast, the NHS pension scheme requires contributions to be calculated on the post-sacrifice salary, with consequential effects upon your benefit entitlement. The NHS pension scheme is a defined benefit schemes, with pension based on earnings over the final three years of the member’s career. In many cases, therefore, a salary sacrifice taken many years before retirement will have no impact upon the pension ultimately payable. However, the life assurance component (death-in-service) would be immediately affected, as would an entitlement to an early pension if obliged to retire due to ill health or seriously disabling injury. The exact details of the College pension schemes vary and you may wish to contact the College Pensions Office for further information, particularly if you are over 50 or are paying/wish to consider paying salary-related Additional Voluntary Contributions. You may also wish to seek independent financial advice. Q8: Will the sacrifice alter my entitlement to contractual benefits provided by my employer, such as occupational maternity pay, sick pay, holidays etc. No. Q9: Will the sacrifice affect my entitlement to state benefits, such as state retirement pension, statutory maternity, adoption, statutory shared parental leave or statutory sick pay. Yes, in some cases it may do so. Where state benefits are calculated by reference to contractual salary or national insurance contributions during or prior to the period of a salary sacrifice, your benefits may be reduced and the College cannot do anything to mitigate or compensate you for any such lost benefits. If this is important to you, you should not enter into a salary sacrifice. You need to be particularly careful if you have only recently joined the College and are not yet entitled to employer’s maternity/adoption/ shared parental benefit. Statutory maternity/ adoption /shared parental benefits are based on recent earnings, and your entitlement could be significantly reduced if you make a salary sacrifice during the eligibility period. Q10: What happens if I join or leave a pension scheme during the sacrifice period. If you join or leave USS or SAUL you need take no action; your pension contributions will be calculated automatically regardless of the salary sacrifice. If you join or leave the NHS pension scheme during a salary sacrifice, please ensure that the payroll office are fully aware of your situation. Q11: Do I have to declare my participation in a salary sacrifice scheme to HM Revenue and Customs? No. All the College’s salary sacrifice schemes relate to benefits which are not taxable. The amount of your pay which is reported to HMRC, and appears on your annual summary of earnings and tax deducted by the College (on form P60) already reflects the amount sacrificed, so no further action is needed on your part. See also Q19, below, concerning Tax Credits. Q12: What happens when I qualify for a salary increase, e.g. cost-of-living pay award or salary increment? Your sacrifice is a fixed or percentage reduction in your salary, and your other terms and conditions are not varied by the sacrifice. Pay increases are calculated on the pre-sacrifice amount. If you receive a promotion, cost-of-living award or bonus during the sacrifice period the post-sacrifice pay will be adjusted automatically to reflect the award. Q13: What happens if I cease to be employed by the College during the sacrifice period. Your sacrifice will automatically terminate on the date you leave the College. Q14: I work part-time. Can I still use salary sacrifice? Yes, as long as your salary is sufficiently large to make the sacrifice effective. (See also Q3) Q15: What happens if I am paid a higher hourly rate for any overtime that I am required to work? The overtime is calculated by reference to your pre-sacrifice salary. However, it is not possible to include variable overtime within the amount sacrificed. If you receive guaranteed overtime, or other regular fixed allowances as part of your remuneration package, this can be sacrificed (subject to the warnings given at Q3, above.) Q16: I am hourly-paid or a casual employee, and so my pay varies from month to month. I have no fixed salary. Can I join the scheme? No. Q17: Will my student loan repayments be affected? If you are repaying a student loan taken out with the Student Finance England, your student loan repayments may be reduced slightly and the repayment period may increase as a result of participating in a salary sacrifice arrangement. This is because your repayments are calculated based on your post-sacrifice salary. Q18. How will membership of a salary sacrifice scheme be reflected in my monthly payslip? Your payslip will show earnings components before any salary sacrifice (eg basic salary, overtime etc.), and then each sacrifice scheme will be shown separately with brackets around the monetary amount, to indicate a minus amount Q19: Could the amount I receive as Working Tax Credit or Child Tax Credit be affected if I join a salary sacrifice scheme? Potentially, yes. If you claim Working Tax Credits you will be expected to disclose the amount of your income in the preceding tax year, and in this instance it is your income after any salary sacrifice has been deducted (i.e. your taxable income as it appears on your form P60). https://www.gov.uk/browse/benefits/tax-credits You may be able to claim extra Child Tax Credits but if so you will need to exclude from the cost of your childcare any amounts paid by your employer or through a salary sacrifice arrangement. You may therefore receive a lower award. HMRC have provided an online tool to enable you to check whether you are better of claiming tax credits or childcare vouchers. https://www.gov.uk/childcare-vouchers-better-off-calculator Q20: My partner’s employer offers a similar scheme. Which one should we join? This outline only provides information on the College’s scheme, and you should seek independent advice before making this choice. Q21: Where can I get independent advice? From a variety of sources, such as your trade union, a Citizen’s Advice Bureau, an independent financial advisor, your accountant or your solicitor. The College cannot give you independent advice. Q22: When should I apply? In order to allow time for paperwork to be processed, it is advisable to apply by the 15th of the month before you wish to join. PLEASE NOTE: For fixed-term salary sacrifice arrangements, it is the responsibility of the employee to renew their application to the scheme before the end of the current sacrifice period. Q23: Who should I contact if I have further questions? Please contact the administrator of the relevant salary sacrifice scheme by following the links in the section, above, headed “Salary Sacrifice schemes at Imperial College”. MAA Last revised: October 2015